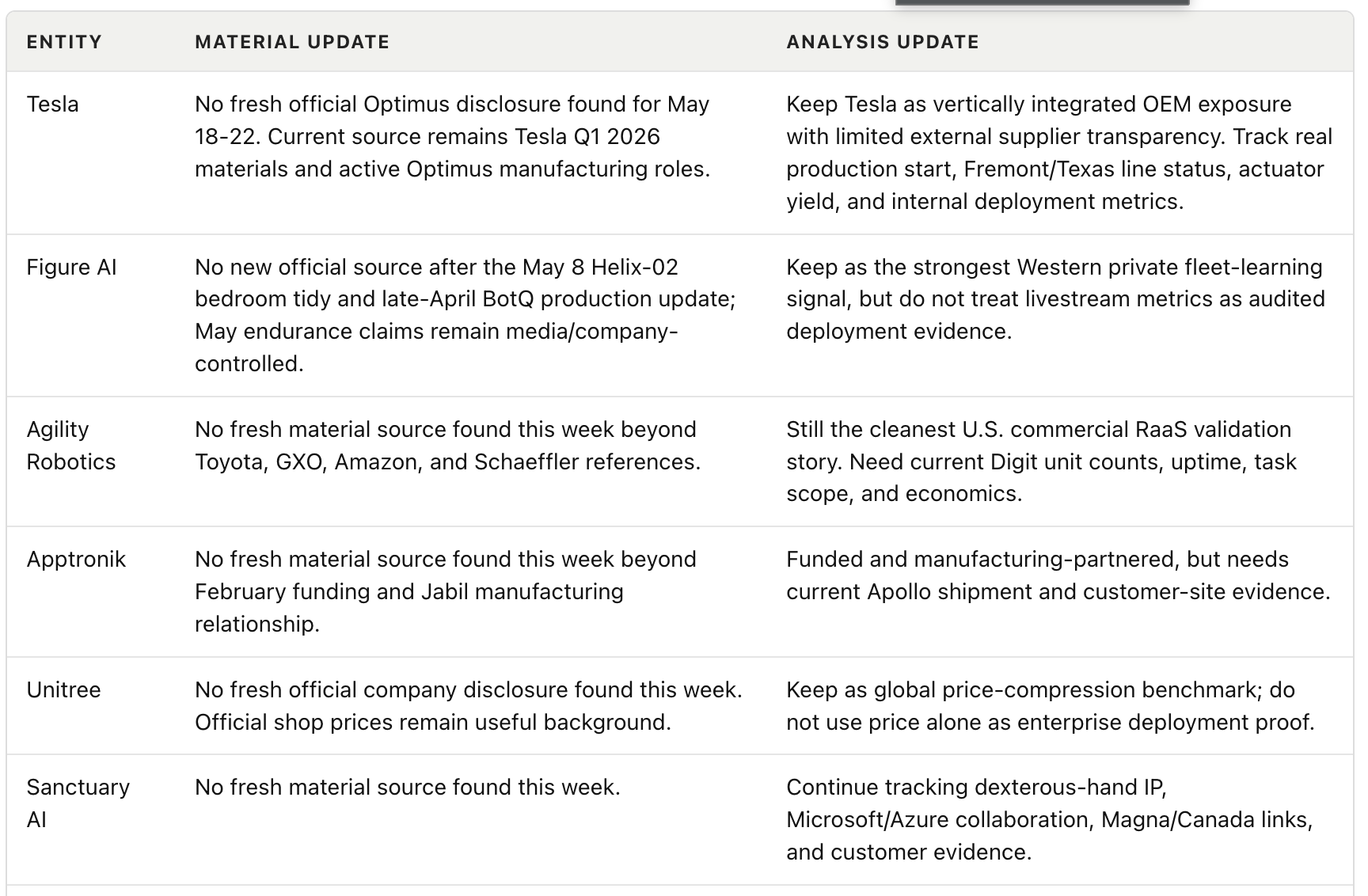

Humanoid Scale-Up Moves From POC to Manufacturing

Humanoid’s Bosch partnership, FANUC and Google’s factory-AI push, and the supplier layers investors should watch next.

The important humanoid signal this week was not another viral robot clip. It was a manufacturing handoff.

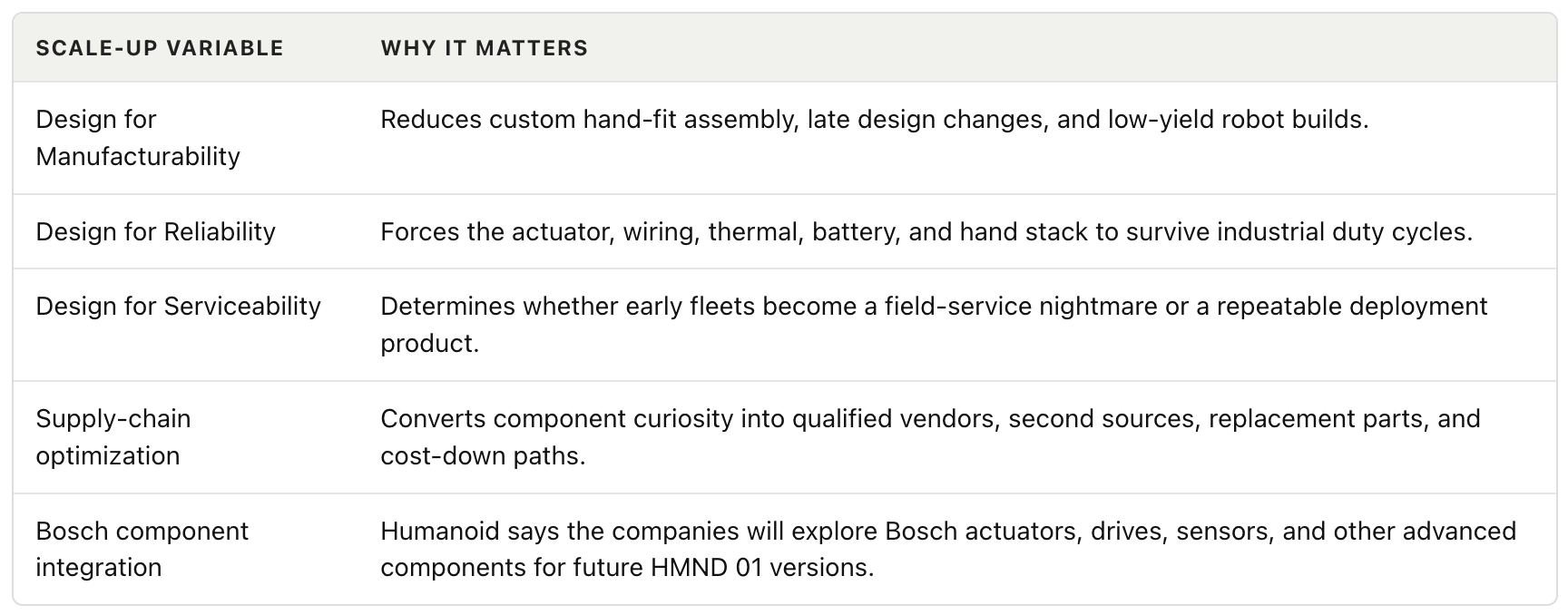

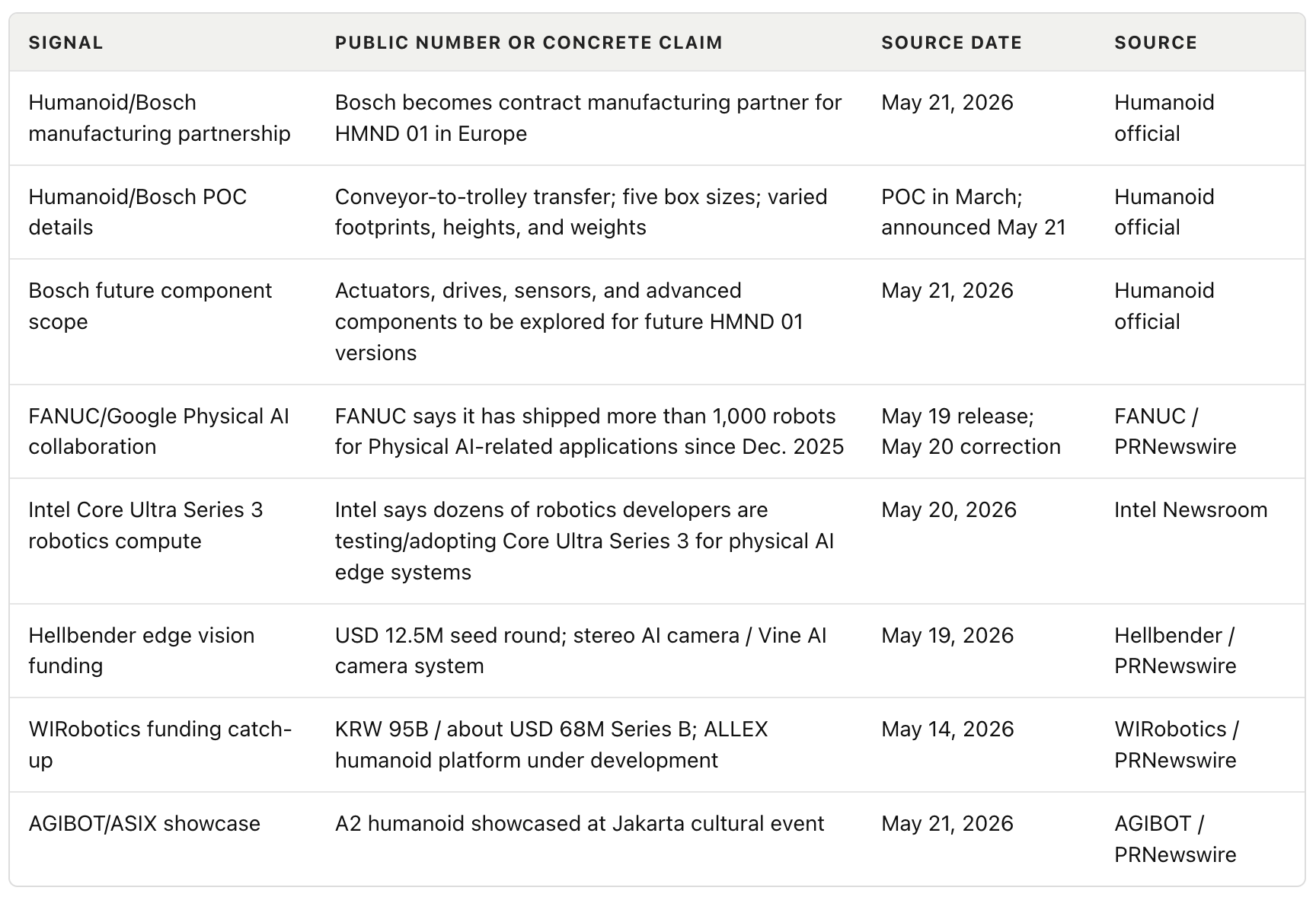

On May 21, Humanoid announced a partnership with Bosch after a March proof of concept at Bosch’s Buhl, Germany logistics environment. The POC was concrete: HMND 01 robots moved boxes from conveyor to trolley, handling five box sizes across different footprints, heights, and weights. The new agreement makes Bosch Humanoid’s contract manufacturing partner for the European market and puts Bosch’s Design for Excellence discipline around manufacturability, reliability, serviceability, supply chain, and cost.

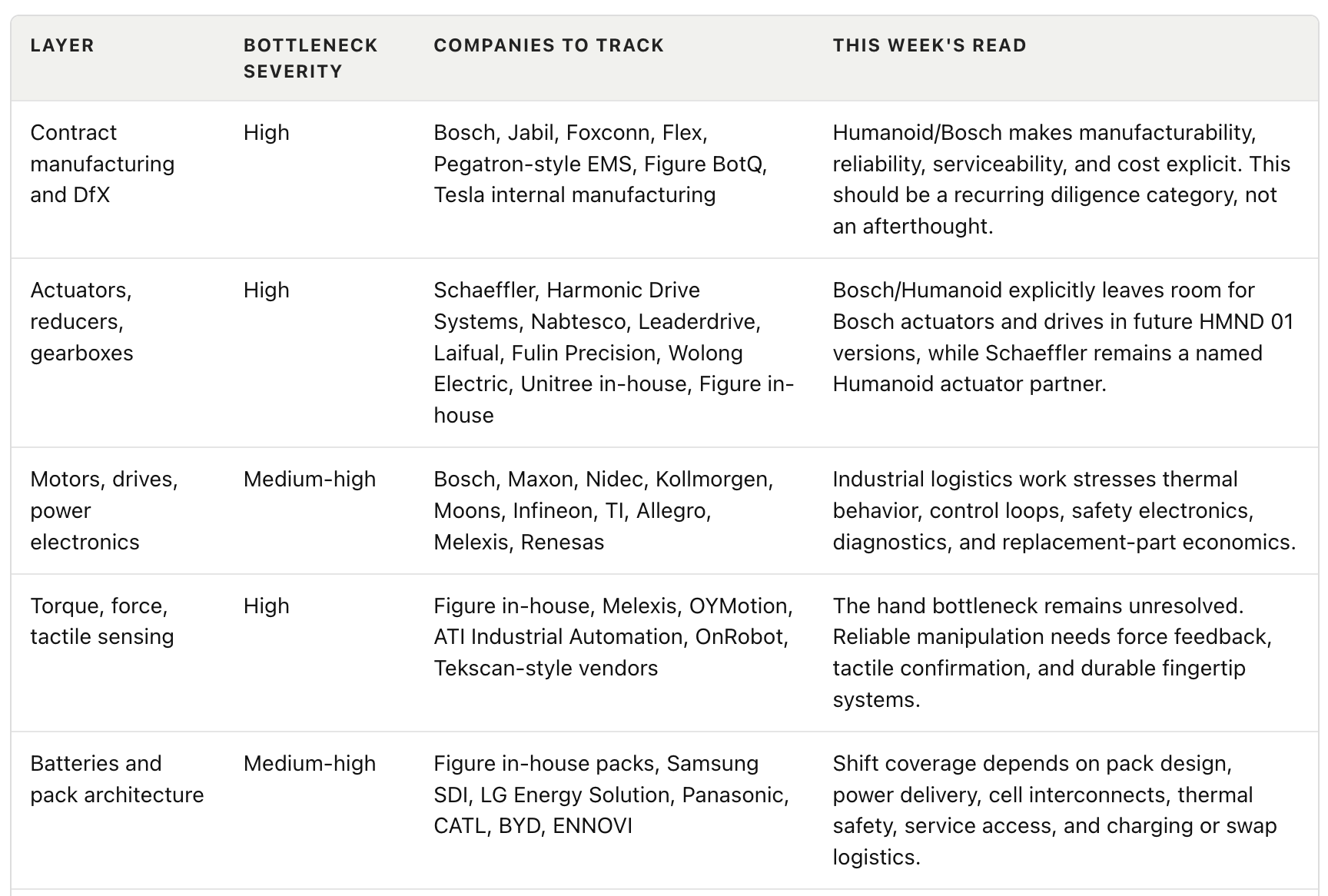

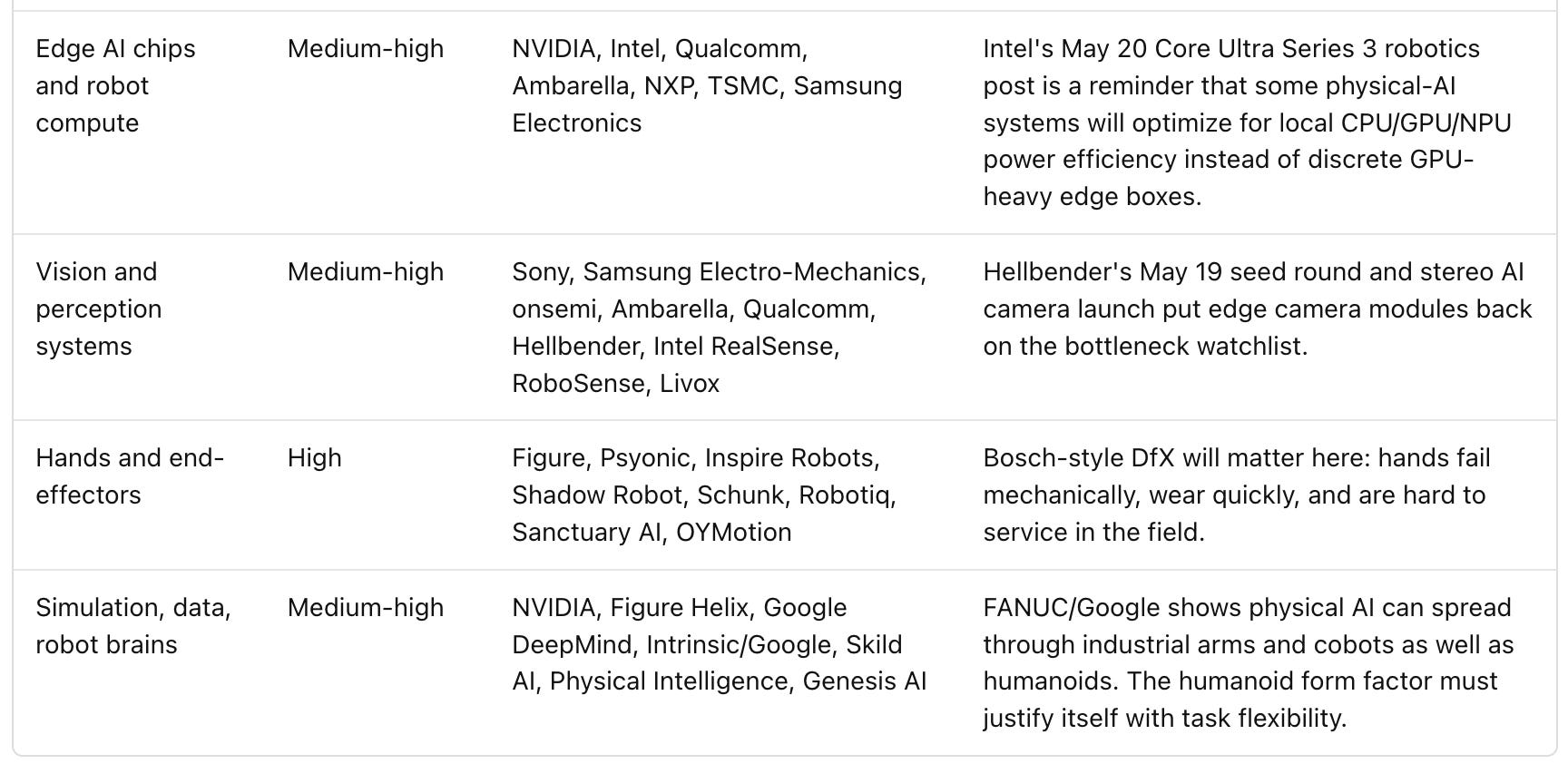

That is the investor signal: humanoid robotics is moving from “does it work once?” toward “can it be built, serviced, costed, and deployed inside industrial systems?” The supplier map widens from actuators and hands into contract manufacturing, DfX, edge compute, edge vision, factory AI, and component qualification.

Subscribe to the Humanoid Alpha for weekly tracking of the public and private companies positioned around the next bottlenecks in actuators, reducers, batteries, edge AI chips, vision systems, hands, simulation data, and manufacturing capacity.

Market signal

Humanoid/Bosch turned a March POC into a May manufacturing partnership.

The key date is May 21, 2026. Humanoid says its March 2026 POC with Bosch demonstrated HMND 01 in an intralogistics workflow at Bosch’s Buhl site, autonomously transferring boxes from conveyor to trolley while handling five different box sizes across varied footprints, heights, and weights. The follow-on agreement makes Bosch Humanoid’s contract manufacturing partner for the European market.

That matters because contract manufacturing is the point where the humanoid story leaves the video layer and starts touching:

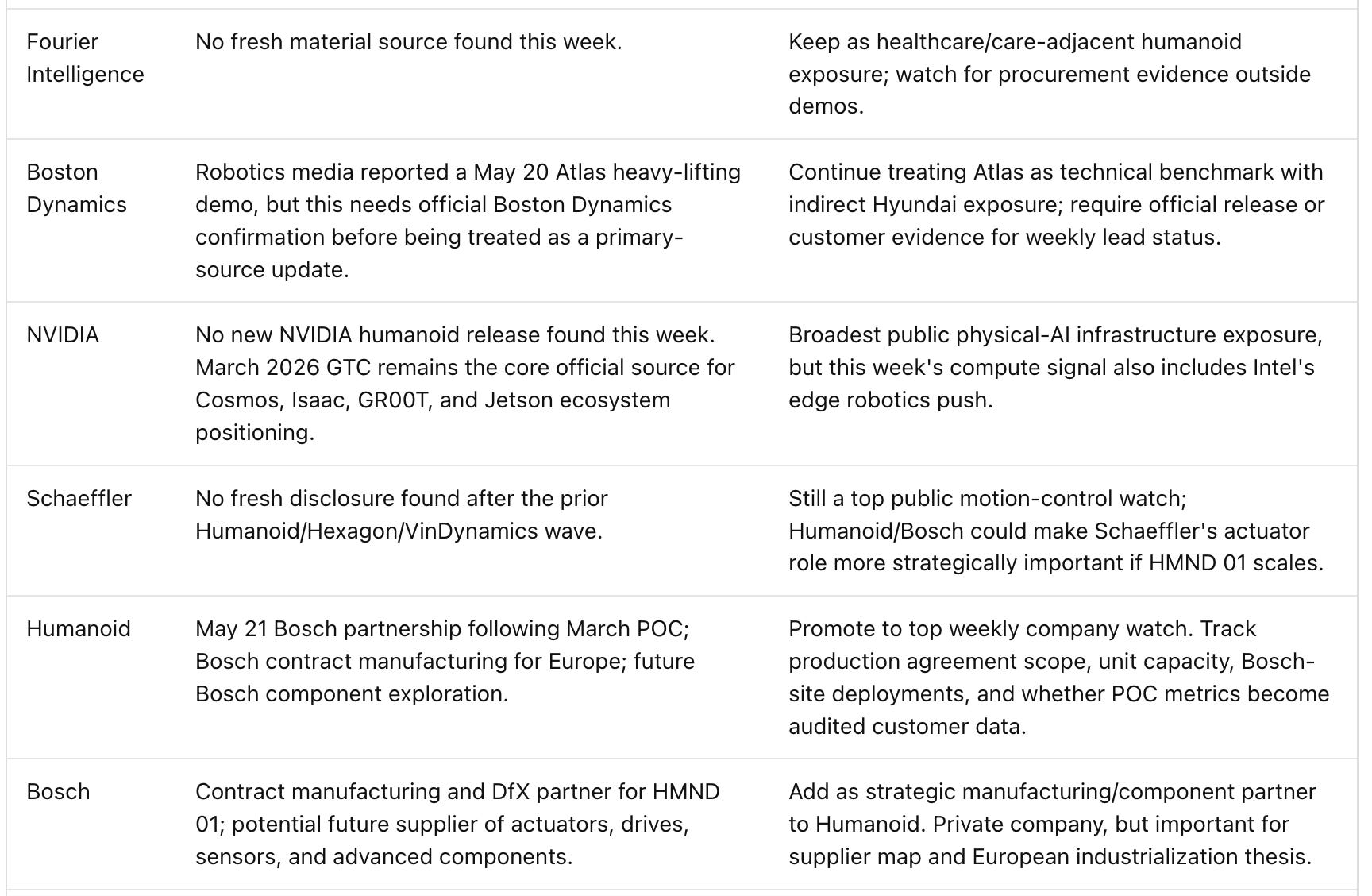

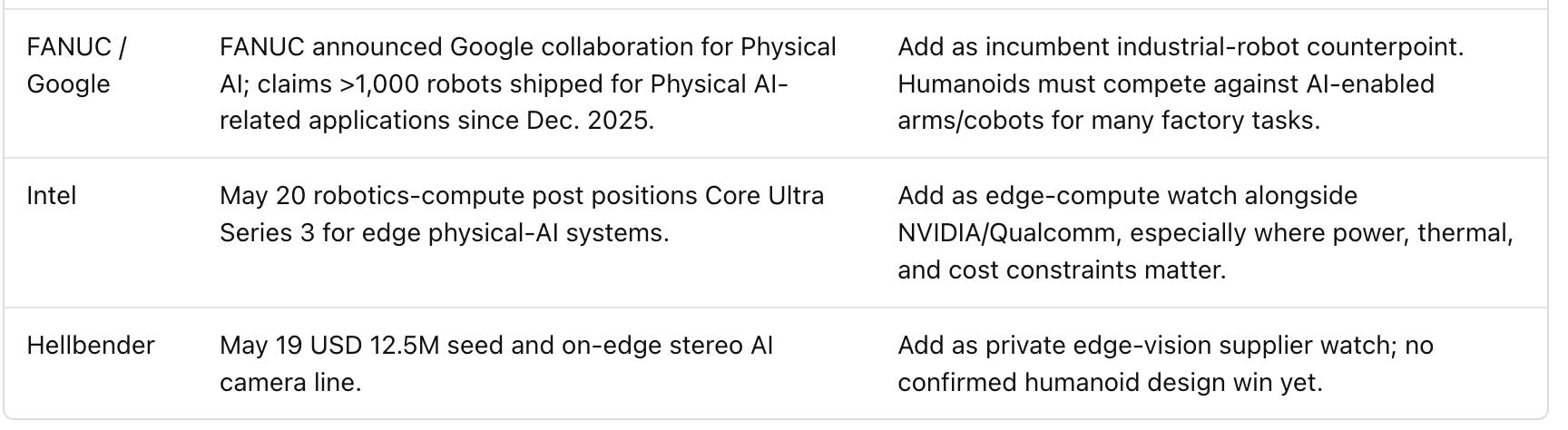

The second signal is that physical AI is spreading into industrial incumbents. FANUC and Google announced a May 19 collaboration, corrected May 20, to advance Physical AI in FANUC robot systems. FANUC says it has already shipped more than 1,000 robots for Physical AI-related applications since the International Robot Exhibition in Tokyo last December. That is not humanoid-specific, but it is highly relevant: factories may adopt AI-enabled industrial robots faster than humanoids unless humanoids prove a clear form-factor advantage.

Company to watch

Humanoid, through Bosch, is the company to watch this week.

Humanoid is still private and early, but the Bosch agreement creates a more investable diligence path than a standalone demo. The right question is not whether HMND 01 looks impressive. It is whether Bosch can help Humanoid move through the industrialization gates that many humanoid programs still avoid naming.

The company-specific watch items:

Can the Bosch partnership produce a repeatable HMND 01 build process for Europe?

Does Bosch become only a contract manufacturer, or also a component channel through actuators, drives, sensors, and advanced modules?

Does the Buhl POC convert into paid deployments, broader Bosch-site use, or customer references?

Can Humanoid publish harder metrics: cycle time, intervention rate, error rate, uptime, box weight range, battery behavior, and maintenance hours?

Does Humanoid’s Schaeffler actuator relationship pair with Bosch manufacturing to form a credible European industrial stack?

The investment read-through is indirect because Bosch and Humanoid are private. The public-market lesson is still useful: humanoid winners may be the companies that can package motion, sensing, compute, reliability engineering, and factory service into a deployable product. That keeps Schaeffler, NVIDIA, Intel, Infineon, Melexis, Jabil, Fanuc, Harmonic Drive-related suppliers, and edge-vision vendors in the diligence set.

Supply chain bottleneck

Manufacturing readiness moved up the bottleneck stack.

Actuators remain the economic center of humanoid hardware, but the Bosch signal says the next gating layer is industrialization: design, yield, service, supply chain, field reliability, and cost-down.

Chart or data point

Recent evidence scoreboard, recency-gated to May 14-22

Investment implication

The near-term humanoid investment thesis should be tightened around industrialization evidence, not headline novelty.

The highest-quality signals now have three traits:

A named industrial counterparty.

A task described in operational detail.

A path from POC to manufacturing, service, or paid deployment.

Humanoid/Bosch scores well on those traits, even though key commercial details remain missing. FANUC/Google is a counterweight: if factory owners can get flexible AI through proven industrial robot platforms, humanoids must earn their place by working in environments where fixed automation and industrial arms are uneconomic or too rigid.

For investors, this favors companies that sell the hard layers regardless of which humanoid OEM wins: precision motion, drives, sensors, edge compute, edge vision, battery interconnects, serviceable assemblies, manufacturing systems, and physical-AI developer infrastructure. The cleaner watchlist this week is Bosch/Humanoid for industrialization, Schaeffler for motion control, FANUC/Google for incumbent factory AI, Intel and NVIDIA for edge/robot compute, Hellbender for edge vision, and Jabil-style manufacturing partners for scale-up.

What changed this week

Humanoid announced a Bosch manufacturing partnership on May 21. The release says Bosch will support HMND 01 production for the European market and provide DfX oversight across hardware design, production, supply chain, and cost optimization.

The Bosch POC was from March, but the manufacturing agreement is the new event. This distinction matters. The POC should be treated as background evidence; the May 21 contract-manufacturing announcement is the actual weekly signal.

FANUC and Google pushed Physical AI into industrial robot incumbency. FANUC says it has shipped more than 1,000 robots for Physical AI-related applications since December’s International Robot Exhibition.

Intel entered the weekly robotics-compute feed. Its May 20 Core Ultra Series 3 post positions CPU/GPU/NPU edge chips as a lower-power alternative to bulky discrete GPU boxes in some physical-AI systems.

Hellbender added a current edge-vision supplier signal. Its May 19 USD 12.5M seed round and AI camera launch are not humanoid-specific, but they are directly relevant to perception bottlenecks in physical AI.

WIRobotics is a useful catch-up, not a fresh lead. The KRW 95B Series B was announced May 14 and should be included only as a late-week funding row unless the next issue finds new deployment evidence.

ROBOTERA should be moved to background. Its May 8 PRNewswire release and earlier late-April/March coverage are outside this issue’s recency window. Keep it in the database backlog, but do not lead a May 22 weekly issue with it.

Structured company and supplier analysis updates

Source links

Humanoid / Bosch May 21 partnership: https://thehumanoid.ai/humanoid-secures-partnership-with-bosch-following-a-successful-poc/

FANUC / Google Physical AI collaboration corrected release: https://www.prnewswire.com/news-releases/fanuc-accelerates-physical-ai-through-collaboration-with-google-302775837.html

Intel Core Ultra Series 3 robotics compute post: https://newsroom.intel.com/artificial-intelligence/intel-core-ultra-series-3-for-edge-ai-robotics

Hellbender seed round and stereo AI camera release: https://www.prnewswire.com/news-releases/hellbender-secures-12-5m-seed-round-to-accelerate-domestic-manufacturing-of-physical-ai-and-launch-its-on-edge-camera-line-302775081.html

WIRobotics Series B release: https://www.prnewswire.com/news-releases/wirobotics-secures-approximately-krw-100-billion-usd-68-million-series-b-funding-302772164.html

AGIBOT and ASIX Jakarta showcase: https://www.prnewswire.com/apac/news-releases/agibot-and-asix-showcase-advanced-humanoid-robotics-at-cultural-event-in-jakarta-302778927.html

Figure BotQ production update: https://www.figure.ai/news/ramping-figure-03-production

Figure Helix-02 bedroom tidy: https://www.figure.ai/news/helix-02-bedroom-tidy

Tesla Q1 2026 update deck: https://ir.tesla.com/_flysystem/s3/sec/000162828026026551/tsla-20260422-gen.pdf

Tesla Optimus manufacturing role: https://www.tesla.com/careers/search/job/staff-manufacturing-engineer-general-assembly-testing-optimus-237957

NVIDIA March 2026 physical AI / robotics ecosystem release: https://investor.nvidia.com/news/press-release-details/2026/NVIDIA-and-Global-Robotics-Leaders-Take-Physical-AI-to-the-Real-World/

ROBOTERA financing and logistics release, background only for this issue: https://www.prnewswire.com/news-releases/robotera-raises-over-usd-200-million-in-new-round-led-by-sf-group-hsg-and-idg-capital-302766752.html

CnTechPost on ROBOTERA late-April reporting, background only: https://cntechpost.com/2026/04/27/embodied-ai-startup-robotera-raises-200-million-new-funding-round/

Not Investment Advise