Harmonic Drive Systems : The Reducer Is the Bottleneck

Harmonic Drive Systems is not a humanoid robot company. That is the point.

Research framing: This is research support, not financial advice. It is not a buy or sell recommendation. Valuation, execution, dilution, competition, timing, liquidity, currency, and cycle risk still matter.

The market is watching humanoid demos.

I am watching the joint.

The demo creates attention. The reducer decides whether the motion can be repeated, scaled, and trusted.

That is why Harmonic Drive Systems (6324.T) is worth a deep dive.

Not because it is a clean way to express “the humanoid future.”

Because it sits near one of the harder physical constraints in robotics:

turning electrical intelligence into compact, precise, reliable motion.

The demo is not the thesis.

The joint is.

What Everyone Is Watching

Humanoid robotics is still consumed as video.

Can the robot walk?

Can it fold laundry?

Can it pick up a tote?

Can it recover after being pushed?

Those videos matter. They recruit engineers. They attract capital.

But they are weak investment evidence by themselves.

They rarely tell you how many takes failed, how hot the actuators ran, how often the hand broke, how much the joint cost, or whether the supplier can make thousands of units without quality drift.

The visible layer is movement.

The hidden layer is mechanical reliability.

That is where Harmonic Drive Systems enters the map.

The Hidden Layer

A humanoid robot is a stack of joints.

Each joint has to convert motor speed into usable torque while preserving accuracy, stiffness, control, and lifetime.

At the actuator level, the simplified chain looks like this:

AI / control policy -> actuator module -> motor + encoder + torque sensor + reducer -> physical motion

The reducer is not glamorous.

It is the component that trades speed for torque.

In a humanoid, that matters because the robot has to move like a machine but interact like a body. It needs joints that can move with precision while surviving impact, vibration, load, and repeated duty cycles.

That creates a hard engineering requirement: compact torque with low backlash.

Backlash is the looseness or play in a mechanical system. Too much backlash and the control loop becomes sloppy. The robot overshoots. The hand trembles. The arm loses precision. The machine looks good in a clip but becomes unreliable in a work cell.

HarmonicDrive is the company’s core answer to that problem.

Harmonic Drive Systems describes HarmonicDrive as a speed reducer generically known as strain wave gearing, with high positional and rotational accuracy. The company also states that HarmonicDrive products are used across industrial robots, medical equipment, optical devices, printing equipment, space development, co-bots, semiconductor wafer transfer robots, LCD panel transfer robots, NASA Mars rovers, and the Subaru telescope (HDS FAQ).

The company product page says Harmonic Drive is compact and lightweight while offering high torque and high accuracy, and lists reducers, gear heads, rotary actuators, linear actuators, motors, optical galvano scanners, sensors, and servo drivers (HDS product list).

That is the important distinction.

Harmonic Drive Systems is not only selling a robot story.

It is selling motion-control infrastructure.

What Harmonic Drive Systems Actually Does

Harmonic Drive Systems is a Japanese precision motion-control company listed on the Tokyo Stock Exchange.

Company profile classifies it as an industrial machinery company and describes the business as precision control equipment and components: speed reducers, rotary actuators, linear actuators, AC servo motors, and other mechatronics products used in industrial robots, semiconductor manufacturing equipment, and other systems. As of the latest FMP profile check, the stock was around ¥7,090, with market capitalization around ¥671 billion (FMP profile, accessed June 7, 2026).

The company itself describes the HDS Group as developing, producing, and selling precision speed reducers and mechatronics products built around them. Its regional structure is also important: Japan, South Korea, Taiwan, and Southeast Asia are handled by Harmonic Drive Systems Inc.; China by Harmonic Drive Systems Shanghai; North America by Harmonic Drive L.L.C.; and Europe, the Middle East, Africa, India, and South America by Harmonic Drive SE (HDS business model).

This is not a one-product microcap. It is a global precision component supplier with exposure to several high-complexity end markets.

That creates both the opportunity and the problem.

The opportunity: if physical AI scales, HDS already has credibility in a component layer robot builders must respect.

The problem: the current business is still tied to industrial automation, semicap equipment, China demand, and customer inventory cycles.

The robot is the headline.

The cycle is still in the numbers.

Why Strain Wave Reducers Matter In Humanoids

Humanoids create a strange mechanical requirement.

They need the torque of industrial machines, but they cannot carry industrial-machine mass.

A factory robot arm can be bolted to a floor. A humanoid has to carry its own joints, batteries, thermal burden, wiring, sensors, and compute.

That changes the reducer equation. The component has to be compact, light, accurate, stiff, efficient, reliable, manufacturable, and qualified for real duty cycles.

This is why reducers are not just “parts.”

They are constraint managers.

In its FY2025 business-results presentation, Harmonic Drive Systems explicitly connects humanoid applications with compactness, light weight, torque, and thinner cup-type designs. The company shows expected applications across dual arms, lower limbs, and humanoid hands, including a typical reducer-axis framing where dual arms can require about 12 axes, legs at least 8 axes, and a five-finger hand about 15 axes (HDS FY2025 results presentation).

The exact reducer count per humanoid will vary by architecture. But the direction is clear: the more degrees of freedom a humanoid needs, the more the actuator supply chain matters.

This is where the thesis becomes investable only if the numbers follow.

Critical component does not automatically mean pricing power.

Critical component plus qualification scarcity, customer urgency, capacity discipline, and margin evidence is the setup.

Without those, it is just a good story.

The Humanoid Evidence

The strongest HDS-specific humanoid evidence is not a named Tesla-style customer list. It is the company’s own language around AI robots and physical AI.

HDS Report 2025 includes a special feature on growth strategy for the AI robot market and another on the Chinese robot market (HDS Integrated Report 2025).

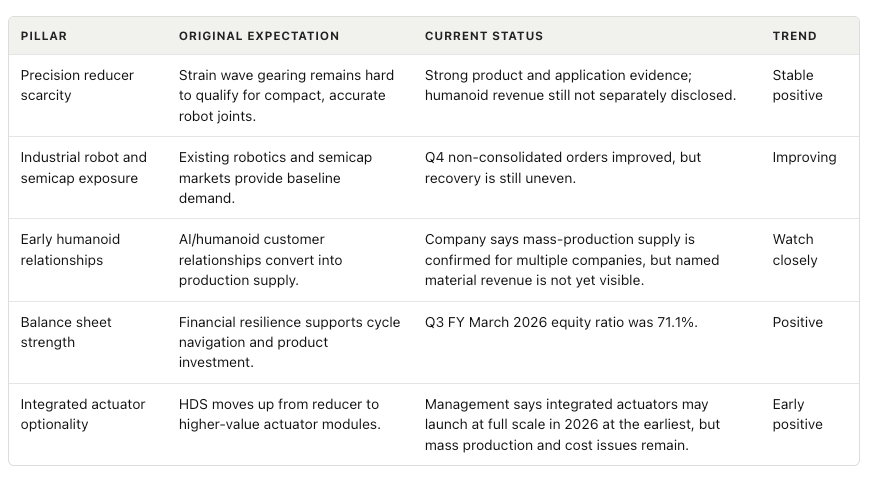

In the Value Creation Story section, management says order volume has been showing a moderate recovery trend after customer inventory optimization, but that end demand has not been as strong as expected. It also says demand for physical AI-related products, including AI-enabled robots, will take additional time before expanding in full swing (HDS Report 2025, Value Creation Story).

That caveat matters. Management is not saying the humanoid boom is already in revenue. It is saying the company is preparing while the market is still early.

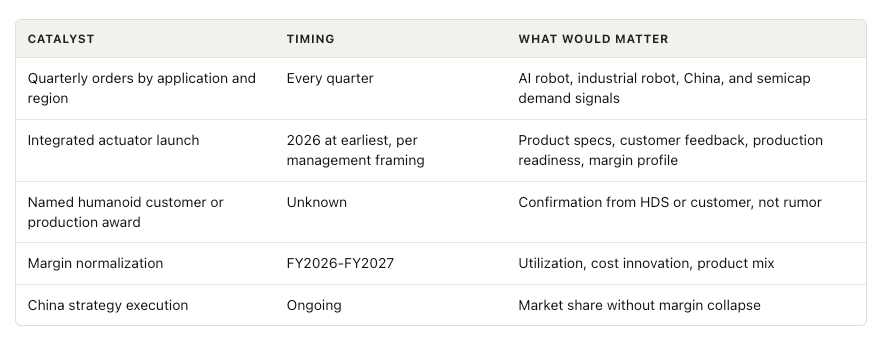

The same report says HDS has seen a steady increase in inquiries and joint-development offers from the physical AI field. It also says the group is focusing on integrated actuators that combine drivers with speed reducers, motors, and sensors, because mobile physical AI systems need more compact configurations than external-driver architectures. HDS says customer feedback has been exceptionally positive and that a full-scale launch could come in 2026 at the earliest, while also noting unresolved issues around mass production systems and manufacturing cost optimization.

That is the right kind of evidence for a watchlist.

Not enough for a victory lap.

Enough to keep the name on the bottleneck map.

The FY2025 presentation goes further. HDS says it developed relationships with players related to AI and humanoid robots in 2024. It also says its current relationships with AI and humanoid robot developers include mass-production supply confirmed for multiple companies, including venture firms, and development collaborations with leading companies exploring entry into humanoids.

That is meaningful. But it is still not the same as disclosed material revenue.

This is the line to respect:

HDS has credible humanoid relevance.

The market may be pricing some of that relevance before the financials prove it.

The Numbers Gate

The financial story is recovery.

Not yet structural acceleration.

For the nine months ended December 31, 2025, HDS reported net sales of ¥42.183 billion, up 4.5% year over year. Operating income was ¥1.191 billion, compared with an operating loss in the prior-year period. Net income attributable to owners of the parent was ¥769 million. The equity ratio improved to 71.1% from 69.5% at the prior fiscal year-end. The company maintained its full-year FY March 2026 forecast of ¥57.0 billion in net sales and ¥1.5 billion in operating income (Q3 FY March 2026 TDnet PDF via JapanIR; JapanIR summary).

The latest HDS non-consolidated Q4 order page is encouraging. HDS reported Q4 FY March 2026 non-consolidated orders of ¥10.605 billion, up 32.1% year over year and 18.0% quarter over quarter. Q4 non-consolidated sales were ¥9.634 billion, up 14.6% year over year and 17.8% quarter over quarter (HDS bookings and sales).

Secondary financial data from StockAnalysis shows FY March 2026 revenue of ¥59.557 billion, up 7.03%, operating income of ¥2.567 billion, gross margin of 30.45%, and operating margin of 4.31% (StockAnalysis financials; StockAnalysis revenue).

This is the crux.

Revenue is recovering. Orders are improving. The balance sheet looks strong. But operating margin is still far below the FY2022-FY2023 levels shown in the same secondary dataset.

That means the market cannot simply say:

“Humanoids need reducers, therefore HDS margins expand.”

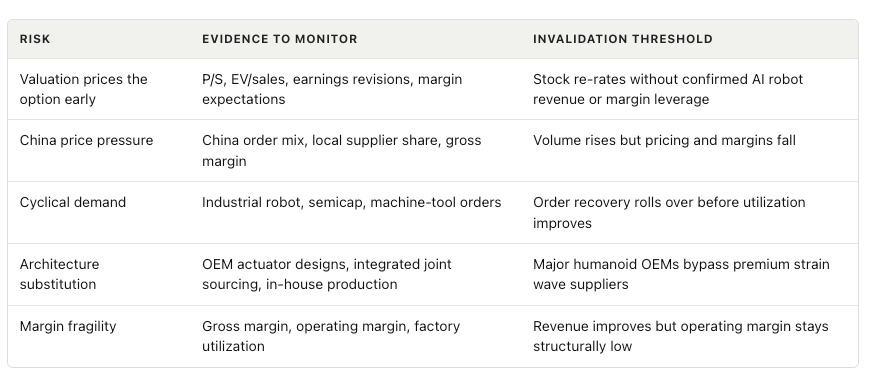

The actual gate is stricter: orders must convert into revenue, utilization must improve, HDS must defend pricing against Chinese competition, integrated actuators must become a higher-value product line, and AI robot demand must become visible enough to offset cyclicality.

Until those questions improve, the thesis is a watchlist setup.

Not a solved case.

The China Layer

China is both the opportunity and the risk.

In HDS Report 2025, management says China remains critical because it leads global industrial robot demand. The company notes that Chinese local manufacturers are becoming a larger share of its customer base, and that HDS has launched initiatives using local components and local assembly.

That is strategically important. It suggests HDS is adapting to the Chinese robot market, not simply defending an old premium position from Japan.

But China-local reducer suppliers can compete on cost, speed, and customer proximity. If humanoid volumes scale in China, local sourcing pressure may increase. HDS says it wants high-value-added products and does not want to compete solely on price. That is the right posture. It is also the source of the investment debate.

If customers prioritize precision, qualification, and reliability, HDS may defend share and margin.

If customers prioritize cost-down at scale, the bottleneck could become a commodity faster than the bull case expects.

Follow the bottleneck.

Then ask who keeps the economics.

Variant Perception

The obvious perception: Harmonic Drive Systems is a robotics supplier that may benefit from humanoids.

The variant perception: HDS is a test case for whether the humanoid market will reward qualified motion-control suppliers before humanoid OEM winners are obvious.

That is different.

I do not need to know which humanoid brand wins to care about the reducer layer.

I need to know whether most serious humanoid designs require high-quality compact reducers or integrated actuators, and whether HDS can capture value as those designs move from prototype to production.

The upside case is not “robots are cool.” The upside case is that humanoid and physical AI developers move from demos to pilot production, actuator qualification becomes harder than investors expect, HDS converts relationships into orders, and utilization plus mix improve margins.

The bear case is cleaner: humanoid volumes take longer than expected, customers redesign around lower-cost suppliers or in-house actuator architectures, Chinese competitors compress price, semicap and industrial robot demand remain cyclical, valuation already assumes the AI robot option, and margin recovery disappoints.

The bull case is a bottleneck story.

The bear case is a valuation and margin story.

Both are real.

Thesis Statement

HDS is a watchlist name for the physical-AI supply chain if humanoid and AI robot demand turns precision reducers from cyclical robotics components into a strategic bottleneck.

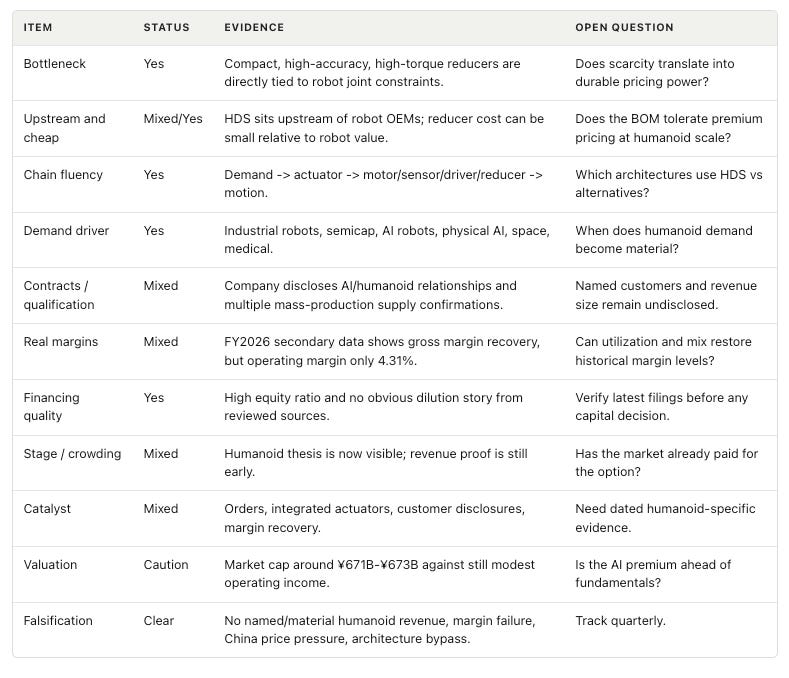

Check List:

Harmonic Drive Systems fits the bottleneck lens.

It is not yet a high-conviction humanoid revenue thesis.

It is a high-priority watchlist name.

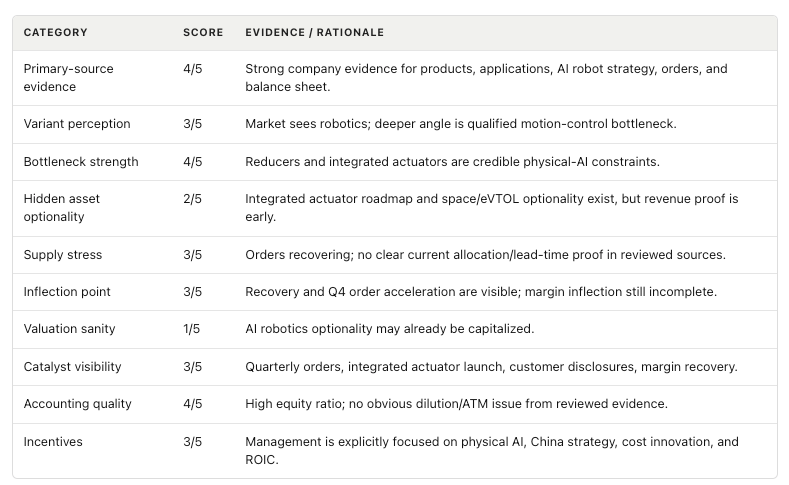

Investment Edge Score

This score is a research aid, not a recommendation.

Final Takeaway

Harmonic Drive Systems is exactly the kind of company deep-tech investors should study. Not because the stock is automatically attractive. Because it forces the right question. I am adding in to my portfolio with a small tracker position.

If humanoid robotics scales, the winner may not only be the company with the best demo.

It may be the supplier that solves the painful, boring, repeated engineering constraint inside the joint.

That is the bottleneck-first lens.

The market is watching the visible layer.

The investor should map the constraint layer.

For HDS, the setup is real enough to track and early enough to question.

Follow the orders.

Follow the margin.

Follow the customer proof.

The robot is the headline. The supply chain is the story.

This article is for research and educational purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any security. The companies discussed may face valuation risk, execution risk, competition, dilution, cyclicality, currency exposure, and timing uncertainty. Always do your own research, verify current filings and market data, and consider your personal risk tolerance before making investment decisions